Money Abroad Guide 2026

How to Send, Receive, Hold and Access Money When You Live Overseas

Handling money across borders can be one of the biggest sources of stress when you are traveling long term, moving abroad, or living between countries. Between hidden bank fees, weak exchange rates, ATM charges, transfers that take days or disappear into fees, it can feel like your money works against you.

That doesn’t have to be the case.

After years of travel and living abroad, I use a system that keeps costs low, moves funds reliably, protects my money, and adapts depending on where I am. I want you to have that clarity too.

In this guide we will cover:

• how to send money internationally

• how to receive money abroad

• how to hold money in multiple currencies

• travel cards and accounts without foreign transaction or ATM fees

• strategies for accessing cash overseas

• practical tips for moving money without tax or bank surprise

• how Wise fits into all of this

I use these tools personally, and they have worked for me in 60+ countries I’ve traveled to without a single foreign transaction issue.

Wise: The Foundation for Moving Money Overseas

If you are sending or receiving money internationally, Wise is the tool I rely on most.

Wise is not a bank. It is a fintech platform built to move money internationally at low cost and at the real exchange rate.

Why Wise Matters

Traditional banks often charge:

• hidden markups on exchange rates

• high transfer fees

• slow delivery times

Wise shows you:

• exactly what fee you pay

• the mid-market exchange rate

• delivery estimates

• the net amount the other side receives

There are no surprises.

How to Sign Up

You can create a Wise account HERE:

With this link, friends get zero fees on a transfer up to $600 on your first transfer. That alone can save you more than choosing a bank transfer.

What Wise Can Do for You

1. Send Money From the US Abroad

Whether you need to pay rent overseas, send support to family, or move savings, Wise lets you send money directly to foreign bank accounts with low cost and transparent pricing.

Wise supports dozens of currencies, including:

• Thai Baht

• Euro

• British Pound

• USD

• AUD

• CAD

…and more.

Unlike banks that take a cut on the exchange rate, Wise uses the true mid-market rate so your money goes further.

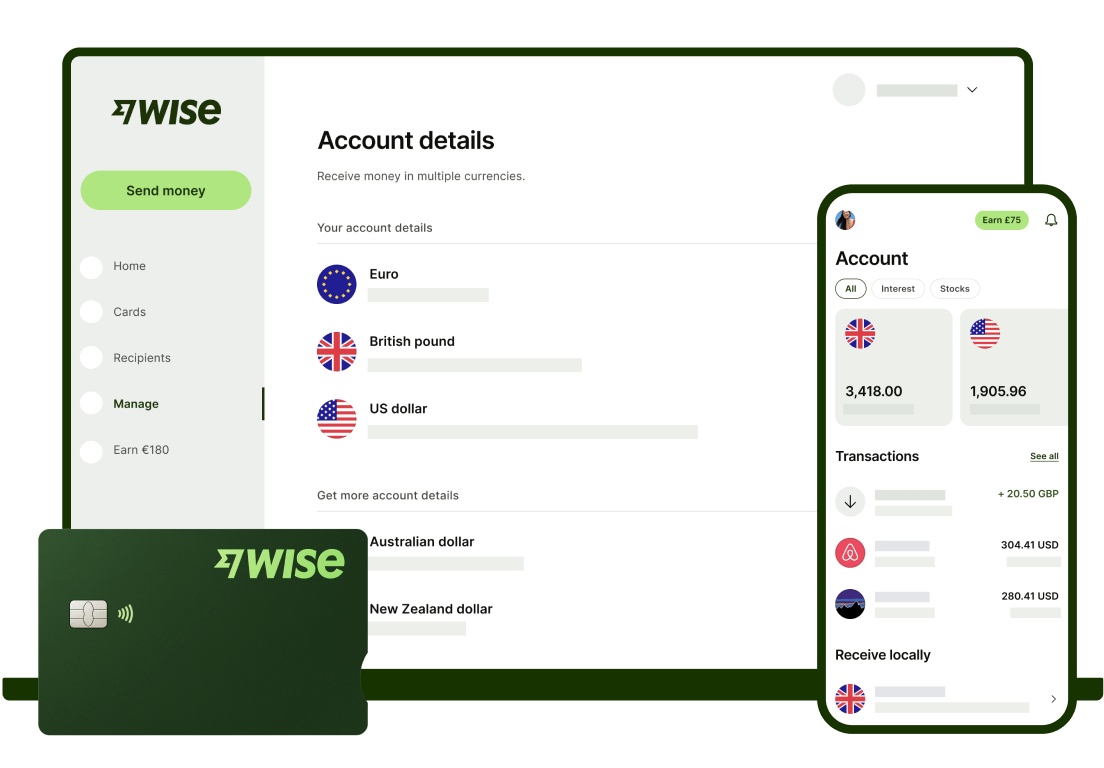

2. Receive Money as If You Have a Local Account

With certain Wise balances, you get local bank details in:

• USD

• EUR

• GBP

• AUD

• and more

This makes receiving money easier without using your home country bank. It is ideal for freelancers, remote workers, and business owners.

For example: someone in the US can send money to your Wise USD balance the same way they send to another US bank.

No international wires. No unexpected fees.

3. Hold Money in Different Currencies

Wise allows you to hold multiple currency balances at the same time.

This is a huge advantage when currencies are moving around due to interest rates, political changes, inflation, or global uncertainty.

You can keep:

• USD

• EUR

• GBP

• THB

• and others

This flexibility lets you:

• hold money where it makes sense

• wait for better conversion opportunities

• spend from a balance without converting

• plan ahead financially rather than reacting

In a world where the strength of the dollar and global markets can fluctuate, holding some money in another currency gives you optionality.

4. Transfer Between Your Own Balances

You can convert between currencies inside Wise as needed. Some people convert gradually rather than all at once to manage risk, especially if they live abroad long term.

Money Management Strategy When Living Abroad

Having the right accounts and cards is only part of it. How you use them matters.

Here is the system that has worked for me:

Layer 1 — Spending

A travel friendly credit card without foreign transaction fees should be your first choice for everyday purchases.

My go-to card overseas is the Chase Sapphire card. I use it in over 60 countries without issues or fees.

If you want to compare offers or apply:

Click here to check it out

Chase Sapphire offers:

• no foreign transaction fees

• travel protections

• strong global acceptance

It keeps day-to-day spending clean.

Layer 2 — ATM and Cash Access

Even with cards, cash is sometimes necessary. Local markets, small vendors, tuk tuks, buses, taxis, and places without card terminals often require cash.

To avoid ATM fees, you want a card that refunds them, and one of the best for this is:

Charles Schwab Bank Debit Card

This card refunds unlimited ATM fees worldwide. Not just some. All.

That means every time you pull cash, Charles Schwab sends the fee back to you.

It also has:

• no foreign transaction fees

• easy online access

• a simple sign up

This changes cash entirely. Instead of avoiding ATMs for fear of fees, you can access cash efficiently and cheaply.

Layer 3 — Transfers and Holding Balances

This is where Wise fits in.

Most people still think:

“my US bank is enough.”

It is not.

Banks are built for domestic money.

They are not optimized for global money.

Wise is.

Use Wise to:

• send international transfers

• receive money abroad

• hold multiple currencies

• make sense of fluctuating rates

If you are paid in one currency but living in another, Wise gives you control over how and when conversions happen.

What You Should Avoid

These common mistakes cost people money:

Using a Bank’s International Wire

Banks often add:

• exchange rate markups

• high flat fees

• intermediary bank fees

The recipient often gets much less than the sender thought.

Using a Foreign ATM Without Fee Protection

ATM fees add up fast, especially when layered:

• ATM fee

• foreign transaction fee

• poor exchange rate

This is why cards that refund ATM fees are vital.

Not Comparing Exchange Rates

A small percentage difference can cost you hundreds over time.

With Wise you see the real rate upfront.

Best Practices When Using Money Abroad

Here are the habits I follow:

Notify Your Banks Before Travel

This prevents random account holds due to “unexpected charges overseas.”

Have More Than One Card

If one card gets declined, you still have another.

Most experienced travelers carry:

• one travel rewards credit card

• one ATM card with fee refunds

Keep Some Cash Global, Some Local

This reduces risk and gives you flexibility.

Use Secure Online Access

Make sure two-factor authentication works when you are abroad.

Multi-Currency Considerations in 2026

Global currency markets are dynamic.

Interest rates, inflation, geopolitical tensions, and economic policy affect:

• how strong your home currency is

• how far your foreign currency goes

• how inexpensive or expensive transfers are

With Wise you can hold money in multiple currencies and decide when to convert based on:

• market conditions

• cost of living where you live

• income currency vs expense currency

This is far more strategic than converting everything right away or leaving all of it in one place.

Quick Comparison: Wise vs Banks vs Other Platforms

Feature | Wise | Traditional Bank | Other FX Platforms |

|---|---|---|---|

Real mid-market rate | Yes | Often marked up | Varies |

Transfer cost | Low & transparent | High + hidden | Mixed |

Multi-currency holding | Yes | No | Some |

Local receiving | Some currencies | Usually no | Some |

Speed | Fast | Slow | Mixed |

Unlike banks, Wise was built for global money. Banks were built for local money.

Final Thoughts

Money shouldn’t be complicated when you are abroad. It should be efficient, transparent, and predictable.

With the right setup — Wise for transfers and multi-currency holding, travel friendly credit cards like those from Chase or Capital One for spending, and a card like Charles Schwab for ATM access — you can strip fees out of the equation and focus on life instead of banking headaches.

Here are the links that help you get started:

Wise (free transfers up to $600 for new users):

USE THE LINK HERE

Chase Sapphire travel friendly card:

USE THE LINK HERE

Money abroad does not have to be confusing. It just needs a strategy.